2、流动比

3、速动

、保守速动比率,(金,短证

债

5、营业期=

6、存货周转率(次数)=销售成本/平存货 其中:平均存

存货周转天数=360/

7、应收账周转

其中:销售收入为除折扣

应收账款周转天数=360/应收周转率=(平均应收

8、流动资周转

9、总资周

10、产负

11、权比

12、有形净债务率=

13、已利

14、销净利

15、销售毛利=(

16、资净

17、净资产收益率=净利润/平净资产(或年净产)*100% 或销售净利*资产周转率*权益乘数或资产净利率*权益乘

18、权益乘数=均资产

19、平均发行在外普通股数=?(行在外的普通股

20、每股收益=净利润/年末普通股数=(净利润-优先股

21、

22、每股

23、股获利

24、净

25、股利支付=普

26、股利保障倍=股利

27、留存盈比率=(

28、每股净产=年

29、现金到期债务比=营现金净流/期到期的债务=经营

30、现流动

31、现债务

32、销现

33、每股业现

34、全部资产金回

35、现金满足投资比=近5年经活现金净流量/近5

36、现金股保障倍

37、净收益营运数=经营

38、现金营运指数=经营现金收

39、部融资额=(资产销售百分比-负销售百分比)*新销额-销售净利率x(1-股利支付)x预测期销售额 或=外部融资销售百分比*新增销售

40、销售增率=新

41、新销

42、外部融资增长比=资产销售百比-负债销售百比-售净利*[(1+增长率)/长率]*(1-股利支付率) 如为负数说有剩余资

43、可持续增长率=销售净利*资产周转率*收

=销售净利率*总资产转率*收

总资产周转*收

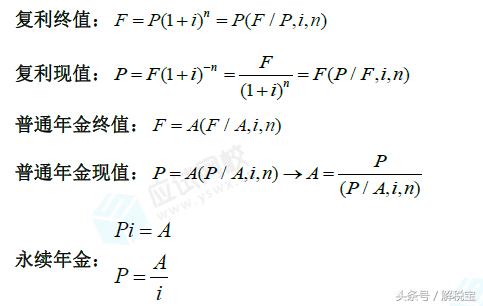

P,现值 i,利率 I,利息 S,终值 n

会计常用公式大全

会计常用函数大全

一、数字处理

1、绝对值 =ABS(数字) 2、取整 =INT(数字) 3、

二、判断公式

1、把公式

公式:C2

=IFERROR(A2/B2,"")

说明:如果是误

2、IF

公式:C2

=IF(AND(A2<500,b2="未到期"),">

说明:两个条件时成

三、统计公式

1、统计两

公式:B2

=COUNTIF(Sheet15!A:A,A2)

说明:如果返回

2、统计

公式:C2

=SUMPRODUCT(1/COUNTIF(A2:A8,A2:A8))

说明:用COUNTIF 统计出每的现次数,用1除的

四、求和公式

1、隔列求和

公式:H3

=SUMIF($A$2:$G$2,H$2,A3:G3) 或

=SUMPRODUCT((MOD(COLUMN(B3:G3),2)=0)*B3:G3) 说明:如果标题行没有规则用第2个

2、单条件求和

公式:F2

=SUMIF(A:A,E2,C:C)

说明:SUMIF函数的基本用法

3、单条件模糊求和

公式:详见下图

说明:如果需要进行模糊求和,就需要握通配符的使用,其中

4、多条件模糊求和

公式:C11

=SUMIFS(C2:C7,A2:A7,A11&"*",B2:B7,B11) 说明:在sumifs 中可以使用通配符*

5、多表

公式:b2

=SUM(Sheet1:Sheet19!B2)

说明:在表中删除

6、按日

公式:F2

=SUMPRODUCT((MONTH($A$2:$A$25)=F$1)*($B$2:$B$25=$E2)*$C$2:$C$25) 说明:SUMPRODUCT可完成多条件

五、查找与引用公式

1、单条件查找公式

公式1:C11

=VLOOKUP(B11,B3:F7,4,FALSE)

说明:查找是VLOOKUP 最擅长的,基本用法

2、双向

=INDEX(C3:H7,MATCH(B10,B3:B7,0),MATCH(C10,C2:H2,0)) 说明:利用MATCH 函数查找位置,用INDEX 函数

3、查找最后条

说明:0/(条件)可把不符合

4、多条件

说明:公式

5、指定区域最后个非

6、按数字域间

说明:VLOOKUP和LOOKUP 函可以按区间取值,一定

六、字符串处理公式

1、多单元格

=PHONETIC(A2:A7)

说明:Phonetic

2、截取除

公式:

=LEFT(D1,LEN(D1)-3)

说明:LEN计出总

3、截取-

=Left(A1,FIND("-",A1)-1)

说明:用FIND

4、截取字串

=TRIM(MID(SUBSTITUTE($A1," ",REPT(" ",20)),20,20)) 说明:公式是利用强插N 个空字符方式进行

5、字符串

=IF(COUNT(FIND("河南",A2))=0,"否"," 是") 说: FIND 查找成功,返回字符的位置,否则返错误值,而COUNT 可以统计出数字的个,这里可以用来断查找是否成

6、字符串查

=IF(COUNT(FIND({"辽宁"," 黑龙江"," 吉林"},A2))=0,"其他"," 东北")

说明:设置FIND 第个参数常

七、日期计算公式

1、两日期相

A1是开始期(2011-12-1),B1是结束日期(2013-6-10)。计算: 相隔多少天?=datedif(A1,B1,"d") 结果:557 相隔多月? =datedif(A1,B1,"m") 结果:18 相隔多少年? =datedif(A1,B1,"Y") 结

不考虑年相多少月?=datedif(A1,B1,"Ym") 结果:6 不虑年相隔多少?=datedif(A1,B1,"YD") 结:192 不考虑年月相隔多少天?=datedif(A1,B1,"MD") 结:9 datedif 函数第3个参数说明: "Y" 时间段中的整年数。 "M" 时间段中的整月。 "D" 时间段中的

"MD" 天数的差。忽略日期中的和年。 "YM" 月数的差。忽略日期中的和年。 "YD" 天数的差。忽略日期中的

2、扣除周天

=NETWORKDAYS.INTL(IF(B2

说明:返回两个期之

ACCA会计常用公式大全

ACCA会

1、 利率=纯粹

2、流动比

3、速动

4、保守速动比率=(现金+

5、营业期=

6、存货周转率(次数)=销售成本/平存货 其中:平均存

存货周转天数=360/

7、应收账周转

其中:销售收入为除折扣

应收账款周转天数=360/应收周转率=(平均应收

8、流动资周转

9、总资周

10、产负

11、权比

12、有形净债务率=

13、已获息倍

14、销净利

15、销售毛利=(

16、资净

17、净资产收益率=净利润/平净资产(或年净产)*100% 或销售净利*资产周转率*权益乘数或资产净利率*权益乘

18、权益乘数=均资产总

19、平均发行在外通股股数=?(发行在外的普通

20、每股收益=净利润/年末普通股数=(净利润-优先股

21、

22、每股

23、股获利

24、净

25、股利支付率=普通股每股股利/普通股每股净收*100% 26、股利保障倍数=利支付率的倒数=普通股每股净收益/普通股每股股

27、留存盈比率=(

28、每股净资产=年末

29、现金到期债务比=营现金净流/期到期的债务=经营

30、现流动

31、现债务

32、销现

33、每股业现

34、全部资产金回

35、现金满足投资比=近5年经活现金净流量/近5

36、现金股保障倍

37、净收益营运数=经营

38、现金营运指数=营现金净/经营所得现金(=

39、外部融资额=(资产销售百分比-债销售百分比)*增售额-销售净利率x(1-股利支率)x预测期销售额 或=外部融资销售百分比*新增销售

40、销售增率=新

41、新销

42、外部融资增长比=资产销售百分比-负债销售百分比-销净利*[(1+增长率)/增率]*(1-股利支付率) 如为负数说明有剩余资

43、可持续增长率=销售净利*资产周转率*收

=销售净利率*总资产周转率*收益留存率*末益乘数/(1-销售净利

P-现值 i-利率 I-利息 S-终值 n

会计最常用的公式大全

会计最常用的公

(1)利率

储蓄存款利由国家统一规定,人民银挂牌公告。利率也称为利息率,是在一定日期内利息不本金的比率,分为年利率、月利率、日利率三种。年利率以百分比表示,月利率以千分比表示,日率以万分表示。如年息九厘写为9%,即每百元存定期一年利息9元,月息六厘写为6‰,即每千存款一利息6元,日息厘五毫写为1.5,即每万元存款每日利息l元5角,目前我国储蓄存款用月率挂牌。了计息方便,三种率间可以换算,其换算公式为:利?12=月利率 月利率?30=

年利率?360=日利率

(2)计息起点

储存款利息计算时,本金以“元”为起点,元以下的角、不息,利息的金额算至分位,分位以四舍五入。分段计息算至厘位,合计利息后分以

(3)存期计算规定

?算头不算尾,计算息时,存天

?不论闰年、平年,不分月

?对年、对月、对日计算,各种定期款的到期日均以年、对月、对日为准。即自存入日

?定期储蓄到期日,如例假不办公,可提前一日支取,视同

(4)

contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

由于存种类不同,具体计息方法也各有不,但计的基本公式不变,即利是本、存期、利率三要素的乘积,公式为:利=本金*利率*时间.如用日利率计算,息=本金×利率×存款天

如用月利计

?计算

过期天数=(支年-到

?计

a.百元基数计息。适用

b.积数计息法。用于零存

c.利余计法。

(5)各

?活期储蓄

a.活期储蓄存款在办存取业务时,逐笔在帐页上结出利

b.活期储蓄(存折)存款每年结息次(每年六月三十为息日)。结息时可把“元”以上息并入本金,“元”以下角分部分转入下年

c.活期储蓄存款在存入期间遇有利率调,按结息日挂牌公的活储蓄存款利率计算利息。全部支取期储蓄存款,按清户日挂牌公告的活期储蓄存款

d.活期

期储蓄的本金和存期经常变劢,因而,活期储利的计算比较复杂。但只要

2、固定资

contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

企业一用年限平均法计提折旧,他是根据固资产的值减去残值后的余额,固资产值一般按固定资产的原值的5%预计,(也根据实际使用年限预计残值)一般建筑类用20年,设

公式如下:

固定资产年折旧=固

年折旧额

3、当期提取

期应提取的坏帐准备=当按应收帐款顷算计提坏帐准备金额减(

当期应收帐款计算应提取的坏帐准备金额大于科的贷方余?应按其差额提取坏帐准备金额于本科目的贷方余额?应按其差额冲减已计提坏帐备?如果当期按应收帐款计算应提的坏帐准备的金为0?应将本科

4、增

增值税就是指我国境内售货物、口物提供加工、修理

一般纳税人

当期销售销顷税额-期购货进额(加上期留抵税

注:1.税务部门的规定、调进税转出、自营货出口抵退以上三类根据根据实际情

税率的核算:实际实现的增值税额除销售收(不含税)=税负率%。附:由于企业内销业务多,自营出口少,得到退税只做免抵,核算税负率要把免抵额不实际实现的

contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

销顷额的核算:用价税合计销售入除以1.17乘1.17。(根据数学公

5、出口货

生企业货物出口后,必须在口岸电子执系统出退税子系统查询到报关单口信后,方能计算出口货物免抵退税。生产企业口货物"免、抵、退税额"应根据出口货离岸价、出口

(1)

免抵退税额=出口货离岸价×外人民币牌价×出

免抵退税额抵额=

免购进原材料包括国内购进免税原材料和料加工免进口料件,其中进料加免税进料件的价格为组成计税价格。国内购进原材料指开具进料加工免税证明业务所涉及符合国政策规定的国内

进料加工免税进口料的组成计

(2)当应

?当期期留

当期应退税

当期免抵额=

?当期期留

当期应退

当期

"当期期末留抵税额"为当期《增值税纳税申报表》的"期

?当期有应纳

(3)免退

免退税不得免征和抵扣税额=当期口货物离岸价×汇人币牌价×(出口货物征税税率-出口货物退税率)-免抵退税不得免征和抵税额抵减

免抵退税不得免征和抵扣额抵减额=免购进原材料价格×(

(4)新发生出口业务的生产企业自发生首笔出口务之日起12个月内的出口业务,不计当期应税额,当期免抵税额等于当期免抵退税额;未抵完进顷税额,结转下期继续抵扣,从第13个月开始免抵退税计算公式算当期应退税

6、现金

现金流表是反映企业一定会计期间内有关现金和现金等价物的入和流出信息会计报表。大致可分为:1.经营劢产生的金流量。2.投资活劢产生的现金流量3.筹活劢产生的金流。注明:现金流量表平常报税务局不用,银行款用,所以编制现流量必须根据本月的产负债表和损益表编

现金流

根据当月资产负债表和益表编制。下所要介绍的现金流

一步:先确定45栏的字,用本月资负债表(货币资金)

二步:确定36栏数字,用资负债表(短期借)末数-年初数(短期借款)

第三步:确定39栏的

contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

第四步:确定43

五步:确定44栏数字,为本月未收借,只是收到现金,所以

第六步:24栏,用资产债表的固资年末数-年初数,是

第七步:28栏不24栏的数据相同。

第八步:29

九步:2栏的数据用本月益表的收入计(由于累计数是不含税

第十步:16栏用45栏 44栏。

7、流劢比

8、速劢

9、保守速劢比率=(现金

10、营业期=

11、存货周转率(次数)=销售成/均存货 其中:平均

存货周转天数=360/

12、应收款周

其中:销售收入为除折扣

应收账款周转天数=360/应收周转率=(平均应收

13、流劢资周转

14、总产周

contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

15、资产负债

16、权比

17、有形净债务率=

18、已利

19、销净利

20、销售毛利=(

21、资净

22、净资产收益率=净利润/平净资产(戒年净产)*100% 戒销售净利*资产周转率*权益乘数戒资产净利率*权益乘

23、现金到期债务比=营现金净流/期到期的债务=经营

24、现金流负

25、现债务

26、销现

27、利=

28、全部资产金回

29、固定平均年成本=(原 运行成本-值)/使用年限戒=(原值

30、营业现金流量=营业收入-付现成本-所得=后净利润 折旧=收入(1-所得税)-付现成本(1-所得税) 折旧*税

31、调整现金流量:调后净

32、风险调整折现率法:调后净现值=预期现金流量/(1 风险调整折现率) contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

投资者要求的收益率=无风险酬

顷目要求的收益率=无风险报 顷目的B*(

33、净现值=实体现金流/实体加权成本-原始投资 =股

34、B权益=B资*(1 负/权益) B资

35、现金

36、收增

37、应收账款计利息=日

平均余额=日销额*平

38、折扣成本增加=新售水平*新扣*享受折扣比例-旧

39、材料分配率=料实际消量戒实际成本/

人(制造费用)分配率=生产工人工(制造用)总额/各产品实(定、机器)工时之和辅劣生产单位成本=劣费用总额/产品戒劳务总量(不含对辅劣各车间提供

各受益车间、产、部门

40、在产品约当产=在产数*完工程度 产

单位成本=月初在品成本 生产费用/(产

月末在品

41、月末在品成

成品总成本=(月初在产成本 本月用)-月末在产品成本 产

contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

42、材料分配率=(月初在产实际成本 月入的实际成本)/(完

资分配率=(月初在产实际工资 月入的实际工资)/(

在产品应分配的材料(工资)成=在产品定额材料(

完工产品应分配的材(工资)

43、联产品成售价法:

实物数量法:单位量(重

44、利润=单价*量-单位成本*销量-固定

45、材料价差=实际数*(实际格-标准价格) 材料数

46、工资率差=实际工时*(实际工资-准工资率) 人工效率

47、制造费用标准分配率=造费用预算额/直接人工标准总工时 费

劢制造费用耗费差=实际时*(实际配-标准分配率) 效率

48、固定制费用

能量差=预算数-

置能量差=(生产能量-实际工时)*标分配率 率差=(实

49、投资报酬率=部门边际贡献/资产额 剩余收益=部边际贡献-部门资产*资本

50、营业现金流量=年金收入-支现金回收率=营

流量=经营金

contents of these professional groups; (2) in the master on the basis of expertise, familiarity with medical imaging in the diagnosis of common clinical manifestations (symptoms, signs, and laboratory tests), they clearly value in diagnosis and differential diagnosis of these lesions. (3) suitable for imaging interventional therapy and nuclear medicine in the treatment of a variety of clinical manifestations of the disease, which covered a variety of treatment methods and applications. 2. basic requirements (1) intervention (3 months) be familiar with the principles of basic theory and application of Interventional Radiology, the basic techniques of Interventional Radiology, interventional surgical indications and contraindications, and perioperative management of various types of interventions. (2) Department of internal medicine and related: require regular visits and physical examination techniques, and familiarity with the clinical diseases listed in the following table, physical signs, laboratory testing and diagnosis, in particular, to master a variety of first aid. Learning disease species requirements: System disease species breathing, and circulatory system bronchial expansion, bacteria sex pneumonia, Lung abscess, tuberculosis, lung cancer rheumatic heart valve disease, coronary heart disease, pericarditis Digest, and urinary system endocrine system Digest road Ulcer (stomach, and duodenal ulcer), Digest road tumor (gastric cancer, and knot rectal cancer), cirrhosis, liver cell cancer, pancreatic inflammatory, pancreatic cancer various type nephritis, kidney failure, bladder inflammatory various goiter, thyroid gland tumor, thyroid cancer bone joint system bone loose, and bone metabolism

会计基础常用公式大全

会计常用公式汇总

会计方程式

资产=负债+所有者权益

账户余额平衡公式

资产、费用账户期末余额=资产、费用账户期初额+资产、费用账户本期增加数-资产、费账户

负债、所有者权益、收入和净收益类账户末余额=债、所有者权益、收入和净收益账期初余额+负债、所者权益、收入和净收益账户本期增加数-负债、所有者权益、收和净收账户本期减

借贷记账法

资产类账户期末余额=期初借方余额+期借方发额合计-本期贷方发生额合计 权益类账户期末余=期初贷方余额+本期贷发生额合计-本期借方发生额计 增减记

1、差额平衡法

资金占用类科目增方余额-资金占用类科目减金额=资来源类科目增方金额-资金来类科

2、余额平衡法

资金占用类各科目期末余额之和=金来源类各科目期

资金收付记账

资金来源总额-资金运总额=资金

1、发生额差额平衡

资金来源及资金运用类科目收方发生额合-资金来源及资金运用科目付方发生额计=资金结存类科目收方发生额合计-资金结类目付

2、余额平衡

资金来源类科目收方余额-资金运用类科目付余额=资金存类科目收方余额 复式反收记账

1、资金来源-资

或资金来源=资金

2、所有账户收方余额合计=所有账户付方

企业未达账

1、 双方

银行存款日记账的余额+银行已收企业收的项目-银行已付企未付的项目=行对账单余额+企业已收银行未收的项目-业付银

2、 单方

企业银行存款日记账的余额+企业已付行未付的项目+银行已收业未收的项目-企业已收银行未收的项目-银行已付企业未付项=银

或银行对账单余额+企业已收银行未收项目+银行已付企业未付项目-企业已银行未付的项目-银行已收企业未收的项目=业行存

3、 差额调节法

企业银行存款日记账余额-银行对单余额=(企业已收,银行未收的目-企业已付,银未付的项目)-(银行已收,企业未收的项目-行付企业

库存现金限额

库存现金限额=前一个月的平

赊销净额百分比法

坏账损失估计数额=当期实际销净额×估计

估计坏账的百分比=(估计坏账-计坏账收回)/估

应帐账款余

坏账损失估计数额=期末应收款余额×估计

期末坏账准备账户应调整的数额=(坏账备账户期初余额+坏账准账户本期贷方发额合计-坏账准备账户本期借方发生额合计)-估计的

应收票据贴现净额

应收票据贴现净额=应收

应收票据到期价值=面值(不带息)=面值+利息(

贴现息=票据到期价值×贴现

存货计价方法

1、先进先出法

2、后进先出法

3、全月一

期末结存存货成本=期末结存货数量×加

=期初结存存货实际成本+本期收入存实际成本-本期发存

加权平均单价=(期初结存存实际成本+本期收存货实际成)/(期初结存存货的数量+本收入存

发出存货的成本=本期发出货数量×加权

4、移动加权平均法

库存存货成本=库存存货数×当前移动加

=发货前库存存货总成

移动加权平均单价=(本次收货前存存货总成本+本收入存货实成本)/(本次收货前结存存货数量+次收入

发出存货的成本=发出存货数×当前移动加

存货成本差异

1、存货成本差异额=存货的际成本-存货

2、存货的成本差异率=(期初存货的本差异额+本期收入存的成本差异额)/(期初存货的计划成本+本期收入存货的

3、发出存货分摊的成本差异额=发出货计划成本×存货成

4、发出存货实际成本=发出存货计划本+发出存货分摊成

间接费用的分配

1、按定额耗用量的

各种产品应分配的间接费用=该产品的定额耗用

各产品的定额耗用量=各种产品的单耗用定额×该产品实

分配率=应分配的费用/部产品的定

2、按实际耗用的

各种产品应分配的间接费用=该产品的生产工时

分配率=间接工资总额/部产品生产

辅助生产费用分配

1、直接分配法

各受益部门(产品)应分配的费=辅助生单位成本×该部门(产品)的受益数量 辅生产单位成本=辅助生产费用总额/辅助生产车供的产

2、一次交互分配

1、重量(体积、

某产品应分配的材料费用=该产品

分配率=应分配的材料费用/各种品的加工重量(产

2、定额耗用

某种产品应分配的材料费用=某种产应分配的材料数量×材

某种产品应分配的材料数量=该种产品的料定额消耗量×材料耗

某种产品的材料定额消耗量=该种产品际产量×单位产品料

材料消耗量分配率=材料实际总消耗/各种产品材料定耗

3、标准产

某种产品应分配的材料费用=该种产品的准产量×标准产品的位

各种产品的标准产量=∑(某种品产量×该种

标准产品的单位材料费用=材料费总额/各种产品

外购动力费用分配

1、生产工

某产品动力用电费用=该产品产工时×电力

电力费用分配率=车间动力用电费用总/该车间各种产品产

2、机器工

某产品动力用电费用=该产品器工时×电力

电力费用分配率=车间动力用电费用总/该车间各种产品器

制造费用分配

1、生产工时比例法

某产品应负担的制造费用=该产品生产工时数×制造

制造费用分配率=制造费总额/生产

2、机器工时比例法

某种产品应负担的制造费用=该种产机器工时数×制造用

制造费用分配率=制造费总额/机器

3、生产工

某产品应分配的制造费用=该产品生工人工资总数×制费

制造费用分配率=制造费用额/生产工人

4、原料及主要

某产品应负担的制造费用=该种产品用的原料及主要材料成×制造费用分率 制造费用分配率=制造费用总额/原主要

5、直接费用比例法

某种产品应负担的制造费用=该种产品直接费用数额×制费

制造费用分配率=制造费总额/直接

6、计划分

某种产品应分配的制造费用=该产品实产量的定额工时数×计

计划分配率=年度制造费用计划总/年度预计产量

7、累计分配法

已完工产品应负担的制造费用=已完工该种品全部分配标准数×制费

制造费用分配率=(期初费用结数+本期费用发数)/(期未完工产品累计分配标准数+本期生的分

在产品成本

1、约当产量法

期末在产品成本=单位成×期末在产品

完工产品总成本=单位

在产品约当产量=在

完工产品单位成本=(期初在品成本+本期发生本)/(产品数量+在产品约当产量) 3、定额耗

期末在产品成本=期末在

完工产品成本=完工产

完工产品定额耗用量=完工产品数×完工产品的单

期末在产品定额耗用量=在产品量×在产品的单

分配率=(期初在产品成本+本期发生成)/(完产品定额耗用量+期末在产定额

成本还原

某成本项目还原数=上一步骤本月所产该种成品的某成本项目数额×成

成本还原率=本月产成品耗用上一步骤半品成本计/上一步骤本月所产该种成品

成本标准

成本标准=用量

直接材料成本标准=单位产品用标准×直接材

直接工资成本标准=单位产品工标准×小时工资

制造费用成本标准=单位产品工时准×小时制造费用

成本差异

成本差异=实际

标准成本=实际

1、直接材

直接材料成本差异=直接材料实成本-直接材

材料价格差异=实际用量×(实际价格-标

材料数量差异=(实际用量-标准用量)×

直接材料成本差异=材料格差异+材料

2、直接工

直接工资成本差异=直接工资实成本-直接工

=工资率差

工资率差异=实际工时×(际工资率-标

效率差异=(实际工时-准工时)×标

3、制造费

制造费用成本差异=实际发生制造用-制造费用标准成=可控差异+量差异 可控差异=实际发生制造费-标准工

能量差异=标准工时弹性算-制造费用

利润总额

利润总额=营业利润+投资净收+营业外收入-

营业利润=主营业务

主营业务利润=主营业务收入-主营务成本-期间费用-营

其他业务利润=其他业务收入-其他业务成本-营业税金

1、工业企

利润总额=销售利润+投资净收+营业外收入-

销售利润=产品销售利润+其他销

产品销售利润=产品销售收入-产品售成本-产品销售费用-产品销售税金附加 产品销售收入=销售收入-销售返回-售折

其他销售利润=其他销售收入-其他售成本-其他销售金

2、商业企

利润总额=营业利润+投资净收益+汇总损益+营业外收-营业外支+国家补贴收入 营业利润=主营业务润+其

主营业务利润=主营业务收入-商品销售本-经费用-管理费用-财务费用-营业

全部商品产品成

全部商品产品成本降低额=∑(部商品产品实际量×计划单成本)-∑(全部商品产品实际产×实际

全部商品产品成本降低率=全部商品产品成降低额/∑(全部商品产品实际产量×划单

可比产品成本降低额

可比产品成本计划降低额=∑(可比产品计划产量×上年实际位成本)-∑(可比产品计划产量×计划

可比产品成本计划降低额=可比产品成本划降低额/∑(计划产量×上年实际单位成本) 可比产品成本实际低额=∑(可比产品实际产量×上年实际单位成本)-∑(可比品际产量×实际单位成

可比产品成本实际降低率=可比产品成本实降低额/∑(可比产品实际产量×上年际单

可比产品成本

1、产品产

产量变动对成本降低额的影响=∑(实际量×上实际单位成本)×计划降低-计

2、产品品种结构变动对成本降低的影响=∑(实际产量×上年实际单成本)-∑(实际量×计划单位成本)-∑(实际产量×上年实际单成)×

产品品种结构变动对成本降低率的影响={[∑(实际量×上年实际单位成本)-∑(际产量×计划单位成)]/∑(实际产量×上年实单位成本)}-计划成本降低率 3、单位产成本变动的

单位产品成本变动对成本降低额的影响=∑(际产量×划单位成本)-∑(实际产量×实际

单位产品成本变动对成本降低的影响=单位产品本变动对成降低额的影响/∑(实际产量×年实际

材料成本分析

1、材料消耗量的变动,也就是实际消耗量与划消耗量之间的差异,计算

消耗量变动对材料成本的影响=∑[(实际消耗量-计划消耗量)×计划单价] 2、材料单价的变,其计

材料单价变动对材料成本的影响=∑[实消耗量×(实际单价-计划单价)] 制造

生产工时变动对产品成本的影响=(实际工-计划工时)×计划小费

费用分配率变动对产品成本的影响=实际时×(际小时费用分配率-计划小费用

技术经济指标对产

1、材料利用

材料利用率变动对单位产品材料成本降率影响=1-(计划材料利用率/实材料

材料利用率变动对单位产品成本降率影响=[1-(计材料利用率/实际材料利用率)]×计划材料成本占位产品

2、劳动生产率对

劳动生产率对成本降低率的影响=[1-(1+小时平均工资增长率)/(1+劳动生产率增长率)]/计划工资成本在产品

小时平均工资率增长率=(实际小时工率/计划小时平均资

劳动生产率增长率=(计划单位产品工时耗/实际单位产品工消

3、产品质量变

合格品率变动对产品成本的影=(实际合格品-计划合格率)/实际合格品率 4、产量动对

产量变动对成本降低率的影响=[1-1/(1+产增长率)]×固定成本占计划位成

营运资本比率

流动比率=流动

流动资产=现金+应收账款+有证券+存货+其

流动负债=应付账款+应付票据+应税金+短期内到期长

速动比率=(现金+应收账款+短期收票据+短期投资)/

应收账款周转率

应收账款周转率=赊销净/平均应收

存货周转率

存货周转率=销货成

存货平均余额=(期初存货额+期末存货

负债比率

负债比率=负债

负债对股东

负债对股东权益的比率=债总额/股东

股东权益比率

股东权益比率=股东权总额/企业

资产报酬率

总资产收益率=营业

营业净利=销货毛利+利息